Major loan options for buyers they should know about. This includes FHA, VA, Conventional and Vacation Properties.

Home Loan Highlights:

- You should be know about the major loan options for buyers that are available.

- There are a number of different loan options available to buyers for the different properties they wish to purchase including vacation and recreational and seasonal property.

- Loan options include VA, FHA, Conventional and Vacation property purchases.

If you’re considering buying a home or property, having a knowledge of basic mortgage options can help prepare you for meeting with a lender. Here are insights you can use to understand basic loan types and how they affect borrowers.

Loan types: Government-backed vs. conventional

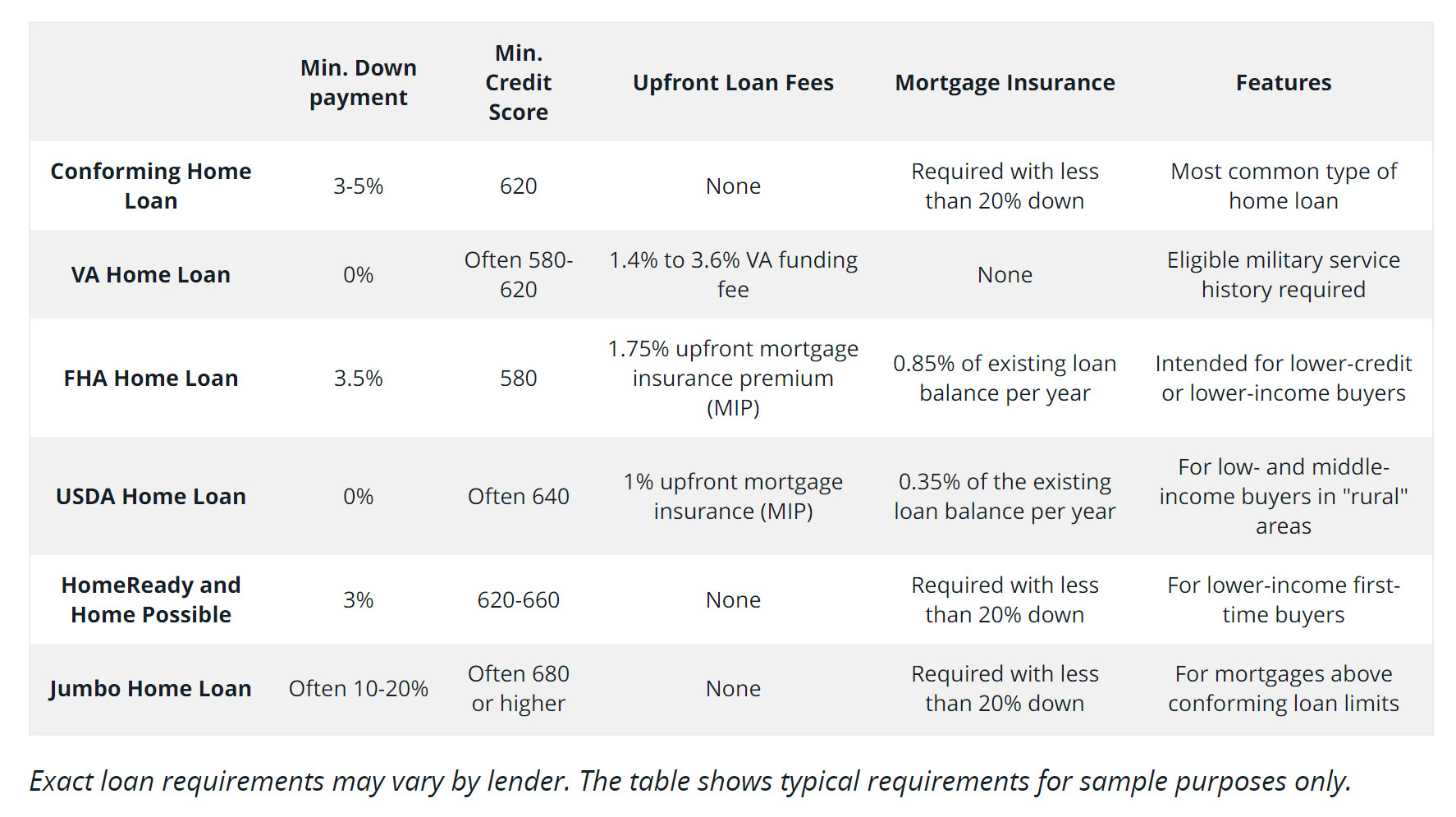

The two different types of loans are conventional loans and government-backed loans. The main difference is who insures these loans:

Government-backed loans:

- Are, unsurprisingly, backed by the government.

- Include FHA loans, VA loans and USDA loans.

- Make up around 40% of the home loans generated in the U.S. each year.

Conventional loans:

- Are not backed by the government.

- Include conforming and non-conforming loans (such as jumbo loans).

- Make up around 60% of the home loans every year.

Government-backed loan types

There are three primary types of government-backed loans: FHA loans, VA loans and USDA loans.

FHA loans

FHA loans, which are insured by the Federal Housing Administration, are typically designed to meet the needs of first-time homebuyers with low or moderate incomes.

Those who take out an FHA loan must purchase a home within a certain budget, the current lending limit for a singled home is $472,030.

Typically the borrower is expected to pay mortgage insurance both at the time of closing and on a monthly basis, and the property must be owner-occupied.

VA loans

VA loans are backed by the Department of Veterans Affairs and they are guaranteed to qualified veterans and active-duty personnel and their spouses. VA loans can be approved with 100 percent financing, meaning VA borrowers are not required to make a down payment.

Unlike FHA loans, borrowers do not have to pay mortgage insurance on VA loans.

USDA loans

You may also hear about USDA loans, which are backed by the United States Department of Agriculture mortgage program. USDA loans are intended to support homeowners who purchase homes in rural and some suburban areas. USDA loans do not require a down payment and may offer lower interest rates; borrowers may have to pay a small mortgage insurance premium in order to offset the lender’s risk.

What’s a conventional/conforming loan?

Buyers who have a more established credit history and a larger down payment may prefer to apply for a conventional loan. These are the most common type of loans. These loans may offer a lower interest rate and only require the home buyer to purchase monthly mortgage insurance while the loan-to-value ratio is above a certain percentage, so a conventional loan borrower can typically save money in the long run.

Vacation Properties

For non-traditional properties, such as seasonal cabins, lake lots, hunting land, hobby farms, water access only properties and other recreational land most local banks will offer “in-house” loans. B.I.C. Realty has a list of local banks that typically finance local vacation properties. It is possible to buy these properties with only 10% down.

Rate types: Fixed-rate vs. adjustable-rate mortgages

In addition to the loan type you choose, you’ll also have to determine if you want a fixed-rate mortgage or an adjustable-rate mortgage (ARM). A fixed-rate mortgage has an interest rate that does not change for the life of the loan, so it provides predictable monthly payments of principal and interest.

An adjustable-rate mortgage typically offers an initial introductory period with a low interest rate. Once this period is over, the interest rate adjusts periodically, based on the market index. The initial interest rate on an ARM can sometimes be locked in for different periods, such as one, three, five, seven or 10 years. Once the introductory period is over, the interest rate typically readjusts annually.

If you have further questions please contact a realtor at B.I.C. Realty and we will be happy to answer questions and put you in contact with professional loan officers who can further assist you.